Page 197 - CW E-Magazine (10-12-2024)

P. 197

Special Report Special Report

Refi nery about 20,000-tpa, for a The fi rst phase of a potentially chain, with these products exported to Renewable carbon feedstocks: Building a net-zero

regional total of 340,000-tpa. multi-phase project would produce Japan.

about 165,000-tpa of blue hydrogen

And this does not include the blue toward the end of this decade, with the Pembina Pipeline/Marubeni JV chemical industry in 2050

hydrogen plant Dublin, Ireland-based hydrogen converted into blue ammonia In May 2023, Pembina Pipeline xperts from nova-Institute, on

Linde, a leading global industrial for export to the Japanese market and Corporation announced it had signed behalf of the Renewable Car-

gases and engineering company, is to possibly others in Asia. a Memorandum of Agreement with Ebon Initiative (RCI), prepared a

build and operate to supply Dow Japan’s Marubeni Corporation for joint groundbreaking report titled “Evalua-

Canada’s Fort Saskatchewan Path2Zero Inter Pipeline/Petronas Canada/ development of a world-scale, low-car- tion of Recent Reports on the Future

project, and Shell’s Polaris project to Itochu JV bon hydrogen and ammonia production of a Net-Zero Chemical Industry in

decarbonize its refi nery and chemical In May 2022, Inter Pipeline Ltd. facility on Pembina-owned lands adja- 2050”. This study, which builds on

plant at Scotford. announced it is partnering with cent to its Redwater Complex in AIH RCI’s pioneering work in introduc-

Japan’s Itochu Corporation and Petro- for export to Japan and other Asian ing the concepts of renewable carbon

Linde has yet to announce the exact nas Energy Canada Ltd. to evaluate markets. and defossilisation, provides a critical Fig. 1: Net zero chemical industry – mean Fig. 2: Net zero plastics industry – mean

capacity of its plant, but said it is to be the development of two facilities assessment of net-zero visions for the feedstock shares (%) feedstock shares (%)

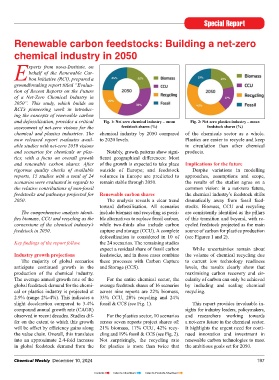

the largest clean hydrogen production to produce world-scale volumes of Initial feasibility studies had been chemical and plastics industries. The chemical industry by 2050 compared of the chemicals sector as a whole.

plant in Canada, and one of the largest blue ammonia and lesser volumes of completed at the time of the announce- now released report evaluates avail- to 2020 levels. Plastics are easier to recycle and keep

in the world, upon completion of its blue methanol for export primarily to ment. The facility has an anticipated able studies with net-zero 2050 visions in circulation than other chemical

two phases near the end of this decade. Japan. design capacity of up to 185,000-tpa and scenarios for chemicals or plas- Notably, growth patterns show signi- products.

As part of Shell’s Polaris project, grey of blue hydrogen production, to be tics, with a focus on overall growth fi cant geographical differences: Most

hydrogen production will be converted Blue ammonia is obviously an effi - converted into about 1-mtpa of blue and renewable carbon shares. After of the growth is expected to take place Implications for the future

into blue hydrogen towards the end of 2028. cient method of transporting hydrogen, ammonia for export to Asia. rigorous quality checks of available outside of Europe; and feedstock Despite variations in modelling

whereas blue methanol serves as a reports, 15 studies with a total of 24 volumes in Europe are predicted to approaches, assumptions and scope,

Proposed export projects versatile building block for numerous Hydrogen Canada Corp./E1 Corpora- scenarios were evaluated in regards to remain stable through 2050. the results of the studies agree on a

In addition, as previously men- everyday productsand is being evalu- tion Partnership the relative contributions of non-fossil common vision: in a net-zero future,

tioned, fi ve consortiums have proposed ated for use as a low-carbon fuel for In October 2023, Calgary-based feedstocks and pathways projected for Renewable carbon shares the chemical industry’s feedstock shifts

world-scale blue ammonia export pro- industries such as shipping. Hydrogen Canada Corp. (HCC) an- 2050. The analysis reveals a clear trend dramatically away from fossil feed-

jects for AIH, with four targeting pri- nounced the closing of its C$10-mn toward defossilisation. All scenarios stocks. Biomass, CCU and recycling

marily the Japanese market and one the Had the project been sanctioned seed round fi nancing and the signing The comprehensive analysis identi- include biomass and recycling as possi- are consistently identifi ed as the pillars

South Korean market. in 2024, the JV was targeting a 2027 of a letter of commitment on an offtake fi es biomass, CCU and recycling as the ble alternatives to replace fossil carbon, of this transition and beyond, with re-

in-service date. agreement with E1 Corporation, a global cornerstone of the chemical industry’s while two-thirds also include carbon cycled feedstock projected as the main

Mitsubishi/Shell Canada JV leader in the LPG industry and South feedstock in 2050. capture and storage (CCU). A complete source of carbon for plastics production

In September 2021, Japan’s Mitsu- ATCO/Kansai Electric Power JV Korea’snumber one LPG provider, to defossilisation is considered in 10 of (see Figures 1 and 2).

bishi Corporation and Shell Canada In April 2023, ATCO and Japan’s develop a world-scale blue hydrogen/ Key fi ndings of the report follow. the 24 scenarios. The remaining studies

Products announced they had signed a Kansai Electric Power Co. announced ammonia facility in AIH for export to expect a residual share of fossil carbon While uncertainties remain about

Memorandum of Understanding to pro- they were collaborating to develop an South Korea and other Asian markets. Industry growth projections feedstocks, and in those cases combine the volume of chemical recycling due

duce blue hydrogen at a facility Mitsu- integrated clean fuels supply chain The majority of global scenarios these processes with Carbon Capture to current low technology readiness

bishi aims to build and start-up near between AIHand Japan. ATCO and Initial feasibility studies with res- anticipate continued growth in the and Storage (CCS). levels, the results clearly show that

Shell’s Scotford complex in the latter Kansai at the time had already com- pect to the blue hydrogen/ammonia production of the chemical industry. maximising carbon recovery and cir-

half of this decade, with Shell/ATCO pleted a pre-feasibility study to produce facility had already been completed by The average annual growth rate of the For the entire chemical sector, the cularity of carbon can only be achieved

providing CO storage via their Atlas blue hydrogen and its derivatives in the HCC, with an anticipated design capa- global feedstock demand for the chemi- average feedstock shares of 16 scenarios by including and scaling chemical

2

Carbon Storage Hub. Heartland, spanning the entire value city of about 1-mtpa of blue ammonia. cal or plastics industry is projected at across nine reports are 22% biomass, recycling.

2.9% (range 2%-4%). This indicates a 33% CCU, 20% recycling and 24%

slight deceleration compared to 3-4% fossil & CCS (see Fig. 1). This report provides invaluable in-

Missed a copy !!! compound annual growth rate (CAGR) sights for industry leaders, policymakers,

For Digital Edition of this month’s issue & all other past issues observed in recent decades. Studies dif- For the plastics sector, 10 scenarios and researchers working towards

Visit www.hpicindia.com fer on the extent to which this growth across seven reports project shares of: a net-zero future in the chemical sector.

PDF copies available for download will be offset by effi ciency gains along 21% biomass, 17% CCU, 42% recy- It highlights the urgent need for conti-

Register Now the value chain. Overall, this translates cling and 19% fossil & CCS (see Fig. 2). nued innovation and investment in

Contact: For Subscription : Mrs. Usha S. - usha@hpicindia.com into an approximate 2.4-fold increase Not surprisingly, the recycling rate renewable carbon technologies to meet

For Advertising : Mr. Vijay Raghavan - vijay@hpicindia.com in global feedstock demand from the for plastics is more than twice that the ambitious goals set for 2050.

196 Chemical Weekly December 10, 2024 Chemical Weekly December 10, 2024 197

Contents Index to Advertisers Index to Products Advertised