30 July, 2024 15:35:27 IST

30 July, 2024 15:35:27 IST

Singapore’s chemical industry has for long been touted as one of the models of efficiency, challenging the classical models for development of the industry. With neither a feedstock advantage, nor a sizeable population to consume locally, the industry has thrived in the City-State by competitively accessing export markets in the region and beyond thanks to world-class infrastructure for manufacturing and logistics, a stable political, if sterile, environment, and proximity to growth markets, notably China.

Singapore’s chemical industry is also reinventing itself, and transforming to a more knowledge-driven business, with focus on advanced materials and life sciences. But it also facing several challenges, some of which are endemic to the chemical industry across the world presently, and others more specific to it. The most important is transitioning to a more sustainable industry, less dependent on fossil fuels, and more so on renewables, for making chemicals and materials, as also for energy production.

As the industry shifts towards using bio-based feedstocks, mono-material packaging, and eco-friendly formulations, Singapore’s chemical industry is repositioning as a sustainable and highly productive hub for chemical manufacturing.

Important industry

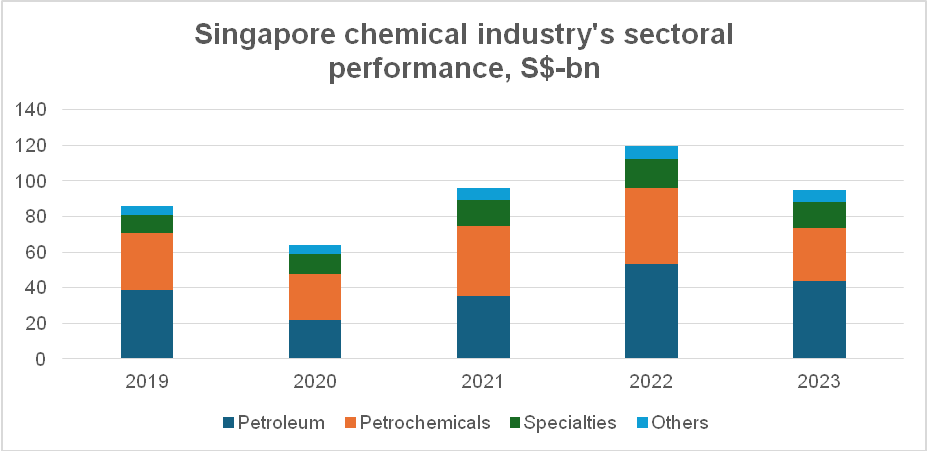

According to the Singapore Chemical Industry Council (SCIC), the trade body that represents the industry, the chemical industry – spanning petroleum, petrochemicals and speciality chemicals – is a very important segment of Singapore’s manufacturing sector, contributing as much as 23% of its overall manufacturing output in 2023. In value terms, output of this cluster of industries in 2023 was about S$95-bn, which was a decline of about 21% from the corresponding figure in the previous year. The contraction seen last year is the largest experienced in recent times, marginally outdoing the 20.5% decline seen in 2020 in the wake of Covid when the country went into a strict lockdown, but some of it can be designated to lower prices.

As Singapore is still a major refining hub, it is no surprise that the petroleum sector has the largest share of chemicals production – accounting for about S$43.6-bn of output (see figure below). This is followed by the petrochemical industry with S$30.1-bn in output in 2023. Together, the refining and petrochemical industries – with a high level of integration between the two – represent about 78% of the value of output of the overall chemical industry. Output of speciality chemicals – with a value of S$16.4-bn in 2023 – accounts for only about 17% of total output, but it is the one sector that has defied overall trends and continued to grow in value each year (including the Covid years) except the last. This is also the segment that the country’s planners are eyeing, in a bid to add further value and to tackle the overbuild of capacity for commodity chemicals in Asia, in general, and China, in particular.

The Jurong cluster – a model for the world

At the heart of the chemicals manufacturing in Singapore is the Jurong cluster – a world-class Chemicals Park that is home to more than 100 of the world’s leading chemical, refining and petrochemical companies. This cluster, which has attracted investments to the tune of S$50-bn over the years, has long been the envy of planners across the world, and has greatly benefitted from the well-thought out integration of refining and petrochemical assets that provide the raw materials needed for several downstream chemicals. The PCPIRs planned for India were to be based on this model, but even after two decades of talks and strategizing there is little to show.

The range of chemicals and related products made in the Jurong Islands presently spans fuels, lubricants, petrochemicals and speciality chemicals, which serve as crucial components in the production of various consumer goods ranging from surgical masks and gloves (which came in handy at the time of Covid) to automobile parts, food flavours and fragrances. The co-location of a terminal to import liquefied natural gas (LNG), to meet the energy needs of the cluster (and beyond), as well as the ‘on-demand’ supply of other utilities (steam, water, industrial gases) as well as waste management facilities, have all contributed significantly to the efficiency of manufacturing operations in the cluster. Tucked away in a corner of a densely populated country, Jurong Island has had an impressive record of safety – a point that planners in India will do well to note.

Tackling the sustainability challenges

Responding to the needs to tackle climate change, and to comply with international regulations, Singapore’s manufacturing sector is required to transition to a low-carbon base. Give that the chemical industry is a significant contributor to carbon emissions and its importance to Singapore’s manufacturing, pivoting this industry to a more sustainable growth path is vital to meet national commitments.

The objective is to quadruple the production of sustainable products from the 2019 levels, and achieve 6-mtpa of carbon reduction through low-carbon solutions by 2050. The Economic Development Board (EDB), which has strategized the growth of the economy through astute planning for several decades now, is expected by 2030 to establish specific targets to transform Jurong Island into a sustainable energy and chemicals (E&C) park. The EDB has awarded S$55-mn to 12 projects under its Low-Carbon Energy Research Funding initiative to support R&D in this space.

Achieving net-zero by or around mid-century, however, won’t be easy. Nearly 95% of Singapore’s energy now comes from natural gas, according to the Energy Market Authority (EMA), and the options for developing more in-country renewables capacity are limited, particularly given the paucity of land. Much of the natural gas has come from neighbouring Indonesia and Malaysia (though recently it has been supplanted by LNG imports from further), but since last year Singapore has also been importing electricity.

Key role for hydrogen

Given the limited options available, Singapore is betting a lot on green hydrogen, produced by the electrolysis of water using renewable energy. The country’s National Hydrogen Strategy is emphasising use of green ammonia – a logistically safer and easier-to-handle carrier of hydrogen – as a fuel for marine transport as well as a source of low- or nil-carbon electricity (when burned in specially modified engines). International partnerships, local technology development efforts and long-term planning are being put in place for hydrogen to play a much larger role in Singapore’s future energy scenario.

Improving resource efficiency and productivity

There is a lot of emphasis on improving resource use – not surprising for a country with limited natural resources. The country today leads in efficient water management and famously recycles municipal sewage back to potable water. Manufacturing companies are also required to assess and account for their water use and to identify, plan and implement measures to achieve water savings through systematic management of the resource.

About five years ago Singapore also introduced a carbon tax scheme, aiming to incentivise emissions reduction while allowing flexibility for cost-effective actions. Over the next decade, the carbon tax will gradually increase towards $50-80 per ton CO2e (carbon dioxide equivalent). Companies are also looking to using Renewable Energy Certificates to fulfil their renewable energy and sustainability obligations. Productivity improvement initiatives in the industry, are calibrating the productivity of companies in Singapore against international benchmarks and facilitating identification of enhancement opportunities.

Several advantages

Amidst extreme commodity price volatility, looming uncertainties in the global economy, oversupply in most chemical value chains and the challenges posed by a transition to a low-carbon world, Singapore’s government has invested heavily in public and private research infrastructure, and skill building.

With strong logistics capabilities, regional connectivity, and comprehensive free trade agreements its over-sized role in chemicals trade will continue. At the epicentre of the Asia-Pacific, the country is well poised to leverage the exceptionally positive demographic fundamentals of the region, which is expected to stay the main driver of chemical demand well into the future.