28 January, 2025 14:40:22 IST

28 January, 2025 14:40:22 IST

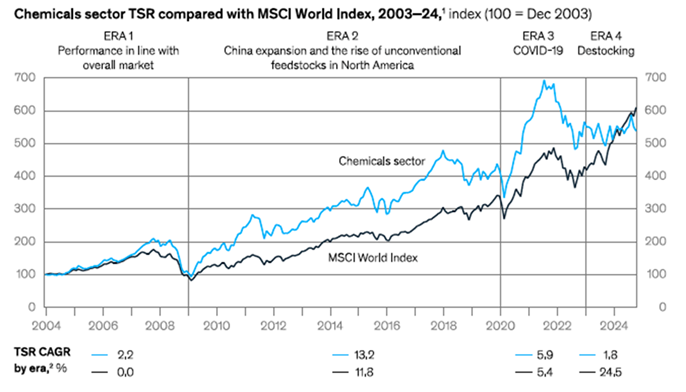

The chemical industry’s value creation to investors has in the last 20 years consistently exceeded the broader capital markets in most major economies, India included. It reached record highs in the aftermath of Covid-19, but since then the story has been very different. As most industry players will assert, profitability in many value chains is now under pressure and total shareholder returns (TSRs) have declined.

A new analysis by McKinsey (The state of the chemicals industry: Time for bold action and innovation)notesthat the industry is entering a new era, evident from the fact that even as global indices have increased 24% per year since late 2022, chemical stocks grew just 2% per year. More worrying is the fear that the change brought about by overcapacity, slowing demand due demographic changes, high energy prices, new regulations& sustainability pressures, and regionalisation, will fundamentally alter the industry’s growth dynamics.

But stakeholders can still significantly enhance value creation by a strong emphasis on innovation, including using the remarkable capabilities that Generative Artificial Intelligence (Gen-AI) provides.

What drove the strong growth?

Several factors contributed to the strong performance of the global chemicals industry over the last 20 years (setting aside the last three). At the top of the list was strong demand, coming from the large populous countries of Asia, notably China and India. The seemingly insatiable demand for base chemicals in China not just drove global demand, but alsoinvestments there,in the Middle East, Southeast & Northeast Asia, and North America. By the end of this period China’s base chemical demand came to account for almost half of global demand, and more than three-quarters of incremental demand. While India too showed strong growth –7-9% per annum in the period – this did not move the needle due the low base (about 2% of global demand).

Access to new feedstocks, notably shale gas in the US, provided ethylene producers a strong cost position. Improvements in productivity, through incremental changes in process technologies, energy management, utilities consumption, byproduct utilisation, as also business process efficiencies, also contributed.

As a consequence of all of the above, in the period from 2003 to 2021, the industry delivered (on an annual basis) TSR of 11%; revenue growth of 5%; and Return on Invested Capital (ROIC) of 14%.

What has changed?

The underperformance of the chemical industry in terms of TSR as compared to the broader market can be attributed to several reasons. For Europe, soaring energy prices in the wake of the Russia-Ukraine conflict has been a key factor. The stocking up of depleted inventories due Covid-19 provided a demand impetus in the post-pandemic years, but that effect has worn off.

McKinsey believes more fundamental changesare now afoot. For one, the industry is reaching the limits of linear demand growth in the developed world. The historical linkage between GDP and chemical industry growth has altered and slower growth is anticipated for the industry. As importantly, capacity additions, mainly in Asia, in the last five years have far exceeded demand growth. Between 2023 and 2028, China is expected to add more than 20-mtpa of ethylene capacity, while annual demand is expected to increase by less than 10-mt. In addition, cost advantaged projects in the Middle East and the US are further putting pressure on margins.

Another significant change is that fundamental innovation appears to have stalled, and many products are commoditising faster than ever before. “The traditional strategy of end-market application tailoring has become increasingly competitive,” says the analysis by McKinsey, lamenting that “the focus has shifted to incremental innovation rather than on designing transformative solutions that address unmet needs for end users and command higher margins.”

The tightening regulatory environment – particularly in Europe – is also a contributory factor, adding complexity and compliance costs.

Creating value through AI

So where does the industry go from here? The identification of new markets, while navigating geopolitical risks,remains vital to growthfor companies inmature economies (not the case in India). The erstwhile approach of expansion by investing in growing Asian markets, especially China, and locating back-office work to low-cost countries (like India), the consultancy says, is outdated, and companies need to look beyond for value creation.

One of the prime drivers for regaining value creation capabilities is through technology, in particular digital innovations, among whichGen-AI is widely seen as game-changing by impacting across business functions. Gen-AIcan process varied sets of unstructured data (such as lab notes, technical specification sheets, scientific literature, and sales presentations) as well as structured data (such as customer relationship management and transactional data) to aid synthesis, suggestions, and new content generation.

Gen-AI-enabled R&D, for example, can be leveraged for optimization of materials, processes, and formulations. In materials, for instance, Gen-AI can enable the development of diverse alloys, crystals and molecules – all without time-consuming and expensive experiments.In drug design, algorithms can help screen the most promising drugs in instants, instead of relying on expensive and long trials, and suggest brand new drugs that do not exist yet, but which are likely to be effective against certain diseases, while still being edible, soluble, etc. For novel formulations,models can be trained to predict the properties of recipes in the making, optimize existing recipes, or generate new ones. McKinsey estimates Gen-AI can provide a more than 30% acceleration in achieving the desired formulation with approximately 5% savings on costs.

In application development, Gen-AI can discover new applications for existing chemicals; significantly reduce the time spent in application identification and developing business cases; and prioritize opportunities based on potential market size and growth. By deeply analyzing vast data sources such as web content, scientific literature, company reports, and market updates, Gen-AI can reveal new opportunities for growth.Gen-AI models can also dive into huge amounts of public data (such as patents, publications, and grants) and suggest chemistries or formulations. The results from lab experiments or scale-up testing are then fed back into the models to further improve the properties. Google DeepMind, for example, has already predicted structures for 2.2-mn new materials, of which more than 700 have been created in the lab and are now being tested.

At an operational level, McKinsey reckons technology-enabled improvements, deploying advanced analytics, sensor technologies and predictive maintenance, amongst others, can add a 5-10% improvement in productivity.

Slow mover

But the chemical industry is still a slow mover when it comes to adopting Gen-AI. A recent McKinsey Global Institute survey estimates that energy and materials, which includes chemicals, has the lowest exposure to Gen-AI tools at 14%, compared with the cross-industry average of 23%. The emphasis still seems to be for back office, supply chain and commercial functions, but that must change if the industry is to improve on its current value creation record.